Why Location Matters for Freelancers Working In These States

Some states are not like the others.

Heads up: the reporting threshold is changing for 2025 and 2026.

It’s tough for contractors to be on top of all the tax law changes from year to year, especially when you’ve got stuff to do like, I don’t know… run a business?

With plenty of changes made to the 1099-K reporting thresholds this year, we brought in tax expert Jonathan Medows, CPA of Medows CPA, PLLC to talk about how it will affect freelancers.

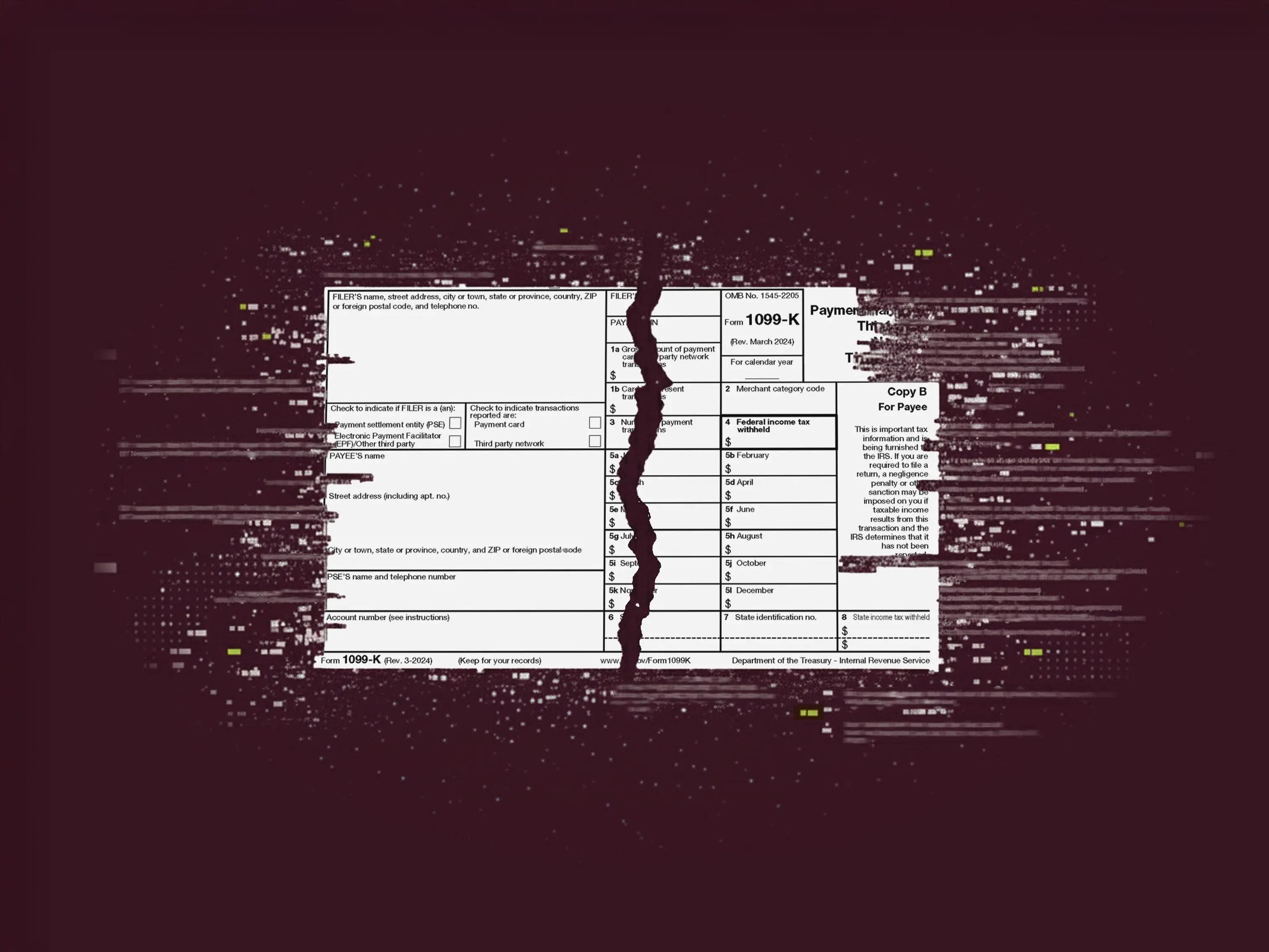

It’s okay if you don’t know what a 1099-K is – there’s seemingly millions of tax forms out there, and it’s easy to confuse them. “When you get paid via a gateway processor [e.g. a payment app like Paypal or VISA], they have to issue a 1099-K,” Medows says. “And they also furnish it to the IRS. The IRS knows you got paid, and it keeps people honest.” If you accept payments through credit card transactions (and you have enough of those transactions to meet the IRS threshold), you should be on the lookout for this form.

If you receive payment through Wingspan (or via direct deposit or as a check), then it’s more likely you’ll receive the 1099-NEC form.

Here’s where it gets tricky. “Some platforms issue 1099-Ks and some don’t,” Medows explains. “Zelle does not. Venmo and Paypal do.” Also, if you are paid less than the 1099-K threshold for the calendar year (more on this later), you also won’t receive the form.

So if you don’t ever receive a 1099-K, does that mean you don’t have to pay taxes on your income? Not so much. “You’re under obligation to report your income,” he says. “After you take out expenses, you need to pay your taxes -- that’s how our federal, state and local government pays its bills.”

Not filing your taxes (and don’t forget to file your estimated taxes as well!) can open you up to potentially painful financial situations. Medows says that the IRS matches third-party data that’s been submitted to them and compares it to what you report on your tax return. If they determine you’re underpaying, their system will spit out a bill that will ask for penalties and interest.

Before the OBBBA passed in July 2025, the IRS said that in 2026, companies paying contractors more than $600 p/year would have to issue them a 1099-K. For workers with multiple clients, that potentially would have created quite a bit of paperwork. But the OBBBA changed all of that.

The new law states that the $600 income threshold is no more. Now, companies will only issue contractors a 1099-K if their total payments are over $20,000 and they’ve received over 200 transactions on a platform during the year. “However, if someone pays you $500 and the client doesn’t issue a 1099-K, the government will not be aware of it unless they were to audit you,” Medows explains. “But you’re still obligated to report it.”

Keep in mind – this new “$20,000 and 200 transactions” threshold also applies for 2025. Why did the threshold change? “From the government’s perspective, this is trying to help the small business operators reduce their compliance costs,” Medows says. “I don’t think it’s to encourage cheaters – everyone is still under obligation to report [the income]. It’s really designed to help small businesses who don’t want to issue [numerous] 1099s – it costs money and time.”

Contractors may have gotten used to receiving a flood of 1099-Ks in their inboxes/mailboxes at the beginning of a new calendar year. With new, higher thresholds on income and transactions, taxes for 2025 and 2026 will likely look different for many workers.

In the midst of all these changes, Medows recommends staying on top of your income taxes by using bookkeeping software that tracks your payments, which will make it easier to pay your estimated taxes. And you can always ask for help from a Certified Public Accountant (CPA) or Enrolled Agent (EA) to make sure you’re paying the correct amount of taxes and filing correctly.

Make things easier on yourself by using Wingspan, which supports your business with invoicing, bookkeeping, and benefits solutions, so you can focus on doing the work you love – learn more.

*This information is not intended to provide, and should not be relied on for, tax or legal advice. Wingspan is not a bank. Banking services are provided by Lead Bank, Member FDIC. Deposits are FDIC-insured through Lead Bank, Member FDIC. The Wingspan Visa® Debit Card is issued by Lead Bank, Member FDIC, pursuant to a license from Visa USA Inc.Your funds are FDIC insured up to $250,000 through Lead Bank.; Member FDIC.

Master your taxes:

When Are Estimated Taxes Due in 2025?

Some states are not like the others.