No items found.

Resource Library

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpg)

.jpeg)

.jpeg)

Compliance

1.1.25

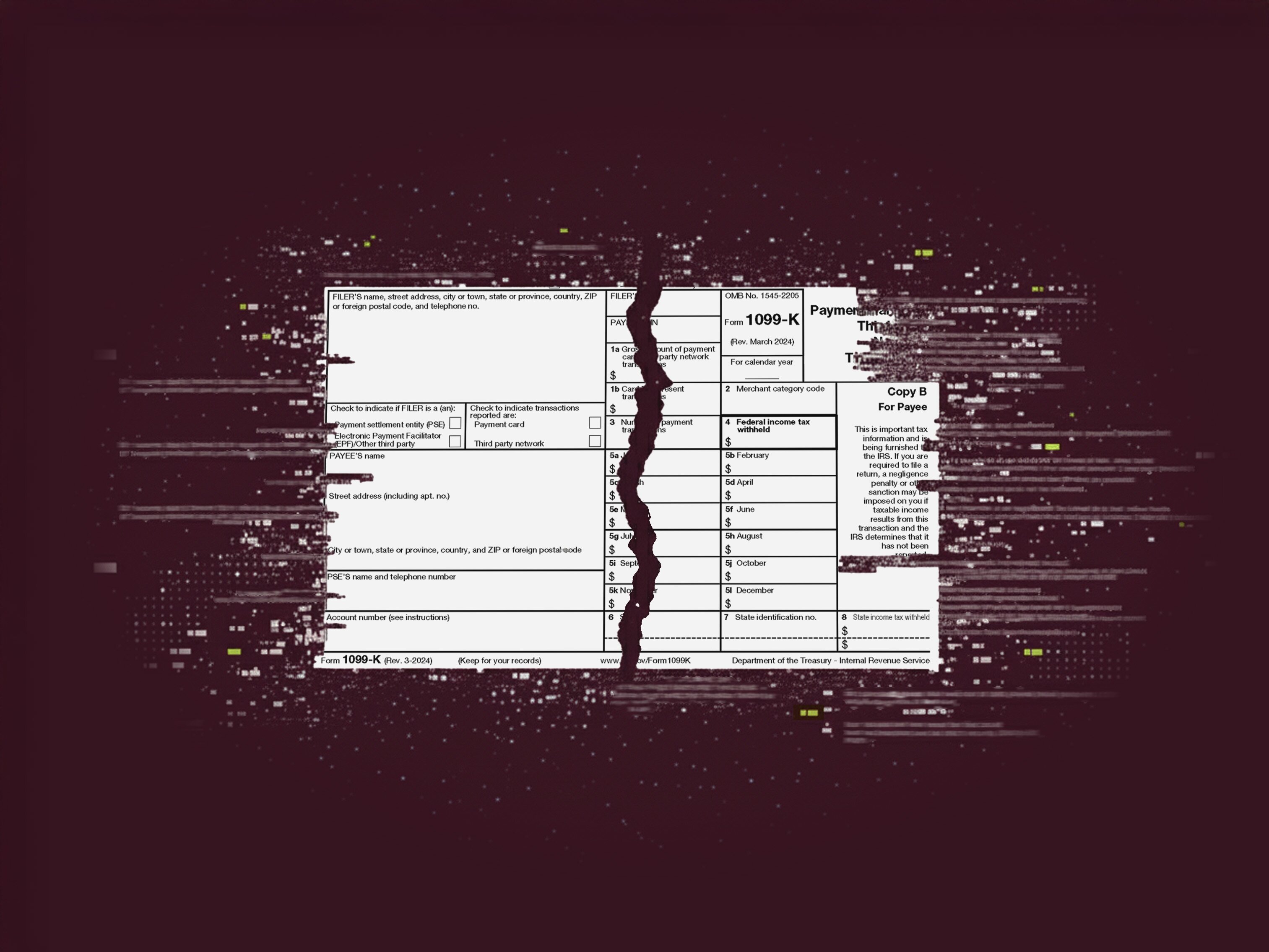

How this telehealth enterprise saved 80+ hours on 1099 management with Wingspan

A fast-growing telehealth enterprise needed a better way to manage the processes behind creating and delivering thousands of 1099 forms to its growing network of mental health providers around the country. They partnered with Wingspan to make it happen.

Compliance

How this telehealth enterprise saved 80+ hours on 1099 management with Wingspan

A fast-growing telehealth enterprise needed a better way to manage the processes behind creating and delivering thousands of 1099 forms to its growing network of mental health providers around the country. They partnered with Wingspan to make it happen.

.webp)

.webp)

.webp)

%20Large.webp)

Payments

11.1.23

Filling financial gaps for gig workers

Fintechs that serve the gig economy are forced to contend with a fractured and diverse landscape. Relevant stakeholders range from gig worker-hiring firms, to HR professionals, to gig workers themselves; building out useful and scalable products requires playing 3D chess, keeping key user cases—as well as shifting regulations—top of mind

Payments

Filling financial gaps for gig workers

Fintechs that serve the gig economy are forced to contend with a fractured and diverse landscape. Relevant stakeholders range from gig worker-hiring firms, to HR professionals, to gig workers themselves; building out useful and scalable products requires playing 3D chess, keeping key user cases—as well as shifting regulations—top of mind

Majestic uses Wingspan to save 100+ hours onboarding and paying 1099 inspectors

5.24.24

The family-owned loss control inspection company recognized an opportunity to use automation to fundamentally rethink the core, and painstakingly manual, processes used to manage its independent inspectors and run its business.